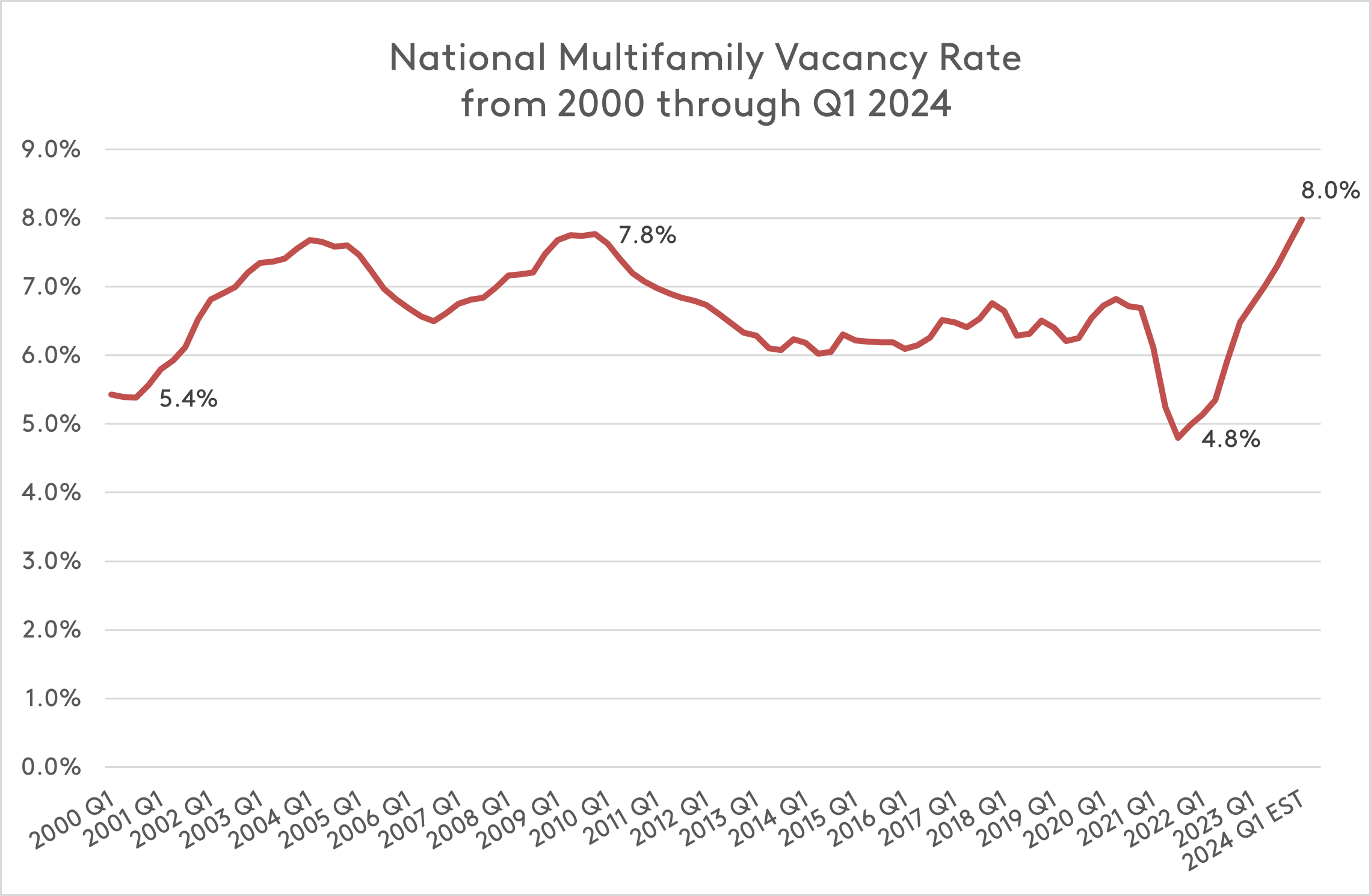

Since their record drop during the pandemic, vacancy rates have been on the rise, pushed up by increasing supply and insufficient demand. The national vacancy rate hit a high of 7.6 percent at the end of last year, and vacancy is on track to rise further in 2024, reaching 8 percent in the first quarter of this year.

As occupancy rates have declined, rent growth over the last two years has decelerated and even fallen into negative territory in the hardest hit markets, such as the Sun Belt, where new construction has been the highest. Currently, 10 major markets lead the nation for above-average vacancy, based on the latest CoStar estimates for the first quarter of 2024.

Multifamily vacancy continues to rise

Zooming out, the national vacancy rate remains elevated even compared to historical data. And following the pandemic-era drop to 4.8 percent, the skyrocketing vacancy rate created the steepest incline of the past two decades.

By asset class, the shift is even more dramatic. Vacancy rates hit 10 percent for four- and five-star apartments at the end of last year, and the luxury class is expected to see 11 percent vacancy this quarter, nearly four points higher than the vacancy rate for mid-priced apartments. Four- and five-star apartments have made up 70 percent of new deliveries, saturating the market and driving double-digit vacancy rates for these high-end properties.

Where is vacancy the highest?

After a spike in in-migration spurred development in the Sun Belt, this region of the country has been overwhelmed by record-high supply. Among the top 10 major markets for highest vacancy, all but one fall in the Sun Belt. These markets have seen double-digit vacancy rates and have posted negative rent growth far below national averages.

1. Austin, TX

At 14.7 percent, Austin leads the nation for highest vacancy, with a rate nearly double the national average of 8 percent.

A top destination for renters moving during the pandemic, Austin saw this demand boom quickly followed by a flurry of new construction. In recent years, demand has cooled as a record number of units have been delivered.

When adjusted for population size, the number of deliveries in this market has been among the highest in the nation. For example, absolute deliveries for Austin in 2023 exceeded those for Atlanta, another oversupplied market, despite the Georgia metro having three times the population of Austin.

Not only does Austin top the list for highest vacancy this quarter, it’s also seen the greatest decline in asking rent among all major markets. Swamped by excess supply, Austin has been struggling with negative rent growth since the second quarter of 2023. At an estimated negative 5.8 percent, rent growth for the first quarter of 2024 is expected to remain in the red, but rent growth in the ATX metro will return to positive territory by the end of 2024, according to CoStar forecasts.

2. Memphis, TN

Struggling with double-digit vacancy, the multifamily market in Memphis falls only behind that of Austin, at an estimated 14.7 percent for the first quarter of 2024. The Tennessee market has faced the unenviable combination of above-average supply alongside below-average demand.

The number of new units under construction in Memphis, while low in absolute numbers, represent the most construction this market has seen in over two decades.

As a result, vacancy rates have remained high over the past five years, only dipping below double digits during the pandemic-era demand boom in 2021 and 2022, though still above national averages.

The second most populous metropolitan area in Tennessee, Memphis is known for its lower-than-average rents, adding to the blues faced by multifamily operators in this music capital.

Despite these challenges, Memphis has seen the smallest year-over-year decline in asking rent of all the major markets in the top 10. Rent growth for the first quarter, while dipping below zero, is expected to be only negative 0.2 percent.

3. Jacksonville, FL

Vacancy rates have been creeping up in this North Florida market, rising from a low of 4.8 percent in mid-2021 to double digits by the beginning of 2023. Estimated to hit 14 percent this quarter, vacancy in Jacksonville is driven by a large construction pipeline.

While demand has been far outpaced by supply, it remains relatively strong, and Jacksonville ranked in the top markets for absorption as a share of inventory in 2023. Boasting strong fundamentals, including a growing population and a robust local economy, Jacksonville is well positioned to return to a healthier balance of supply looking ahead, although the pace of recovery may be slow.

Rent growth, currently at an estimated negative 3.3 percent for this quarter, is expected to end the year in the black.

4. Raleigh, NC

With 13 percent vacancy, the multifamily market in Raleigh is facing record-high vacancy, driven by record supply. Although demand has been positive over the last year, it has been swamped by deliveries nearly double Raleigh’s historical average.

The high vacancy rate in the North Carolina capital has driven rent growth down to an estimated negative 3.2 percent for this quarter.

5. Charlotte, NC

The second North Carolina market to make the top five, Charlotte has seen an estimated 12.5 percent vacancy rate in the first quarter of 2024. What’s driving the high apartment vacancies in the Carolinas’ largest metro? Charlotte is currently facing 30,000 new units under construction. This total represents nearly a seventh of the total inventory and is one of the largest deliveries on record.

Depressed by high inventory, rent growth for the first quarter is expected to drop to negative 2.4 percent and isn’t expected to recover until the fourth quarter of this year.

6. Atlanta, GA

Like many Sun Belt metros, Atlanta was among the top destinations for pandemic migration and is now struggling with an apartment oversupply. The Atlanta apartment market is facing an estimated vacancy rate of 12.4 percent for the first quarter of this year.

In January, metro Atlanta posted one of the greatest year-over-year drops in asking rent among major markets, behind fellow Sun Belt markets Austin, Orlando, Jacksonville, and Charlotte. Rent growth for the first quarter is expected to hit negative 3.0 percent.

Despite its high supply outpacing demand, Atlanta remains one of the most popular cities for renters, based on rental searches in 2023, and the Georgia capital is expected to see rent growth rise in late 2024, as construction starts fall and deliveries taper off.

7. San Antonio, TX

With one of the fastest rates of expansion among major U.S. markets, San Antonio has seen high deliveries not met by demand. In 2023, the flood of new deliveries was the second highest on record for the Alamo City, and the elevated construction pipeline is expected to continue through 2024 and into 2025. This mismatch of supply and demand has driven the vacancy rate to 11.9 percent in the first quarter of 2024.

Rent growth in San Antonio fell into negative territory in mid-2023 and asking rents have remained in decline since. Year-over-year rent growth for the first quarter is estimated to be negative 1.5 percent. CoStar predicts that the Texas metro will return to positive rent growth by the third quarter of this year.

8. Orlando, FL

Supply and demand remain out of balance in Orlando market, contributing to vacancy rate of 11.7 percent in the first quarter of 2024. Home to Disney World, this Florida market remains a popular destination for tourists and residents alike, and in the past five years, it has seen population growth nearly three times the national average. Orlando ranked in the top 10 cities for renter searches last year.

With a heavy construction pipeline, Orlando has seen rapid development that has especially overwhelmed its four- and five-star apartments. Over 90 percent of its new apartment deliveries are in the luxury class.

As of the latest estimates for the first quarter, rent growth remains depressed at negative 3.2 percent, and in January the market saw one of the largest year-over-year declines in asking rent.

Despite these challenges, the Orlando market offers optimistic prospects for the long term, with both renter demand and asking rents expected to grow.

9. Salt Lake City, UT

The only non-Southern metro to rank within the top 10, Salt Lake City is currently facing a vacancy rate of 11.5 percent. The Utah market hit a vacancy rate in the double digits in mid-2023 and is expected to see vacancies rise through 2025. An aggressive development pipeline, paired with economic uncertainty among renters, has caused vacancies to surge.

Asking rents in Salt Lake City, which have declined by 1.2 year over year, have dropped at a somewhat lower rate than most of the markets on this list. However, this drop marks the first time the average apartment rent in Salt Lake City has declined since 2010.

10. Nashville, TN

Another Sun Belt that attracted a flood of new residents during the pandemic, Nashville has seen high vacancy through 2023 and into 2024. Facing strong headwinds, the multifamily market in the Music City has remained volatile, with strong supply-side pressure pushing up the vacancy rate to 11.5 percent.

As a result, rents have declined year over year by 2.1 percent. This negative growth rate is expected to continue through the middle of this year, with the greatest pressures on the luxury class, as mid-priced apartments see tighter vacancy rates.

Where is multifamily vacancy headed?

Driven primarily by the glut of supply in recent quarters, the latest spike in vacancy is expected to slow in the quarters and years ahead. The rate of new deliveries is on track to ease in 2024 and 2025, offering multifamily operators the opportunity to see rents grow — even in challenged Sun Belt markets.

Looking for more multifamily insights?

For more CoStar data and analysis, check out these recent articles and webinars:

- 5 Predictions for the Multifamily Market in 2024

- February Rent Growth Remains Sluggish

- Q4 Increase in Demand Still Not Enough to Meet 2023’s High Supply

- Video: State of the U.S. Multifamily Market: 2023 Recap & 2024 Outlook

What is Apartmentology?

Your source for multifamily insights, Apartmentology brings you the latest data and analysis from industry experts.