webinar

Apartments.com

Important notice:

Due to the CoStar team shifting resources to cover California wildfires, this month’s webinar will not be available. We apologize for the inconvenience.

To ensure you still receive the key insights from this session, we have prepared a written summary of Jay Lybik’s market analysis, which you can read below.

Thank you for your understanding.

Rent Growth on Track to Accelerate in 2025, As New Deliveries Decline

Even as demand rose in 2024, it was swamped by a record number of multifamily units delivered. But with a slowing construction pipeline, 2025 offers some positive signs for multifamily market recovery.

Jay Lybik, national director of multifamily analytics for CoStar, shared the top takeaways from last year’s performance and the outlook for the quarters ahead.

Supply outstripped demand in 2024

The U.S. multifamily market staged a strong demand rebound in 2024, as full-year absorption rose by 70 percent over 2023 to 557,000 units. Renter household formation increased, thanks to slowing inflation, rising consumer confidence, and diminished concerns of recession.

Although the rise in demand was significant, it wasn’t enough to match the 675,000 new units delivered, which marked the highest number of units completed since the mid-1980s.

CoStar’s current projection for 2025 shows demand pulling back to pre-pandemic levels. But risks are leaning toward the upside, which means that new household formations could run above average, if the stable economic outlook continues and new supply remains limited.

Vacancy and rent growth show signs of stabilization

Last year’s imbalance between supply and demand pushed the vacancy rate higher, from 7.7 percent at the end of 2023 to 8.0 percent in December. As a result, 2024 was the third consecutive year in which supply outpaced demand.

In 2025, the vacancy rate is expected to hold steady for most of the year, before edging lower, in possibly the first sign of stabilization coming to the multifamily market.

At the same time, the national average in year-over-year rent growth has remained steady. Rent growth closed 2024 at 1 percent, where it has hovered since mid-2023, following its rapid acceleration in 2021 and 2022.

As market conditions grow more balanced in 2025, this could be “the best opportunity in three years” for national rent growth to once again begin expanding, Lybik said.

“Look for rent growth to expand nationally from the current 1-percent pace to the mid-3 percent range over the next four quarters,” Lybik said.

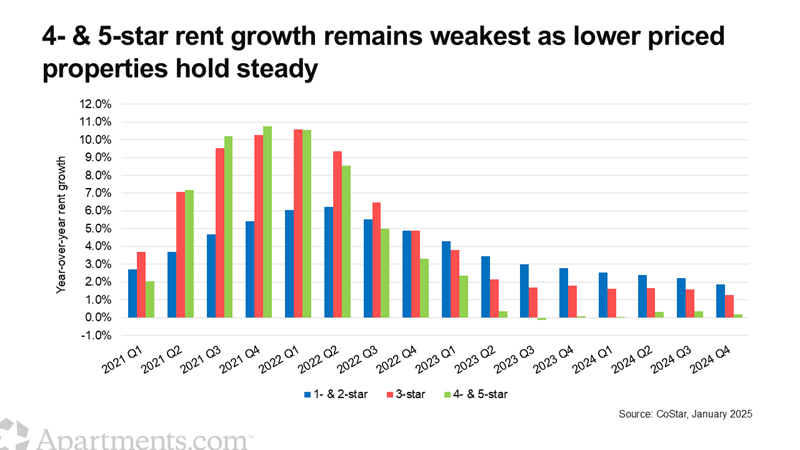

Luxury properties bear the brunt of oversupply

The luxury category has seen the greatest supply-demand imbalance, as this class makes up 70 percent of all units under construction. Oversupply conditions have slowed rent growth for four- and five-star properties the most, with rent growth for top-end properties barely positive in the fourth quarter at 0.2 percent.

Thanks to more balanced conditions in the middle of the market, three-star (also known as mid-priced) properties posted rent growth of 1.3 percent, outperforming the national average.

In 2025, three-star properties are on track to continue to outperform the top end of the market. Excess luxury supply will continue to weigh on operational results.

Relief for the top end of the market could begin in earnest during 2025. After overall completions peaked at 675,000 units last year, deliveries this year are expected to drop by as much as 50 percent.

High vacancy rates drive up concession use

Lybik also addressed a question submitted by a webinar registrant. Autumn Knight in Spokane, WA, asked: “How are property managers utilizing move-in specials and incentives?”

The use of concessions has skyrocketed over the past three years, Lybik said, as apartment owners and operators struggle with oversupply conditions.

In June 2022, only 7 percent of units offered some type of concession. By January 2025, this number is up to 39 percent, which is a 14-percentage point jump from just a year ago.

“There’s no doubt that property managers have significantly increased their use of incentives to raise occupancy,” Lybik said.

For comparison, only 17 percent of units offered concessions before the pandemic, he said.

Sun Belt markets face greatest challenges

In the past three years, Sun Belt markets have seen the largest oversupply conditions. As a result, all of the 10 highest vacancy markets are in the Sun Belt, with vacancy rates ranging from 15 percent in Austin to 11.3 percent in Houston.

Rents fell by 4.8 percent year over year in Austin. The hardest-hit market in the Sun Belt, Austin was joined by Denver, San Antonio, Jacksonville, and Phoenix in the bottom five major markets for rent growth. With the exception of Denver, all are in the Sun Belt.

Only five major Sun Belt markets — Fort Lauderdale, Houston, Miami, Palm Beach and Tampa — finished the fourth quarter with positive rent growth.

In 2025, Sun Belt markets will continue to underperform. However, as multifamily deliveries slow, these markets will have the opportunity to begin soaking up excess units.

The markets with the largest year-over-year declines in deliveries are in the Sun Belt. Dallas-Fort Worth, Austin, Houston, Atlanta, and Phoenix are expected to see the greatest drops, ranging from 19,200 to 10,700 fewer additional units than last year.

The Midwest and Northeast retain their edge

Thanks to the relatively balanced conditions in the Midwest and Northeast, these regions have outperformed the nation with high rent growth and low vacancy.

Detroit, a Midwest market, took the top spot for annual asking rent growth, with 3.2 percent. Kansas City and Cleveland came in second and third at 3 percent and 2.8 percent, respectively.

In 2025, the Midwest and Northeast regions are expected to continue outperforming the nation.

Outlook remains positive, despite downside risks

Currently, the biggest downside risk to the positive multifamily outlook for 2025 is the possibility that an expanding conflict in the Middle East could reignite inflation. An economic supply shock from higher oil prices would significantly dent consumers’ purchasing power and confidence, Lybik said.

If this occurs, it could hurt multifamily demand right when market conditions appear poised for expansion.

“Hopefully, this can be avoided,” Lybik said, “and the U.S. economy will continue expanding throughout 2025, keeping the multifamily recovery on track.”

Explore more resources

For more multifamily market analysis, check out these recent articles:

What is Apartmentology?

Your source for multifamily insights, Apartmentology brings you the latest data and analysis from industry experts.